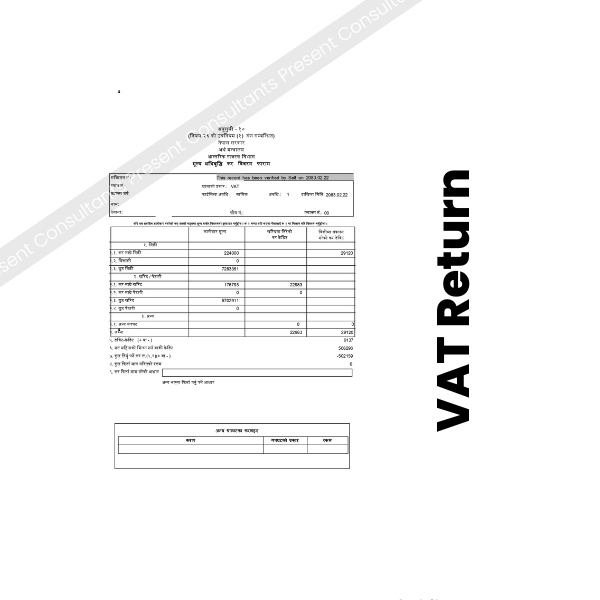

Pursuant to Section 18(1) of the Value Added Tax Act, 2052, read in conjunction with Rule 26 of the Value Added Tax Rules, 2053, every registered person is legally obligated to submit a comprehensive tax return for each designated tax period (typically monthly) within 25 days of the close of that month. Taxpayers must meticulously maintain a standardized Purchase Register (खरिद खाता) and Sales Register (बिक्री खाता) as explicitly prescribed under Rule 23 and Inland Revenue Department Directives. According to these rules, returns must be filed digitally through the IRD portal regardless of whether any taxable commercial transaction occurred during that specific month, resulting in a mandatory “Nil Return” filing requirement.

Failing to submit your returns or settle your outstanding indirect tax balances within the legal deadlines triggers immediate financial penalties and severe administrative sanctions under Chapter 8 of the Act. Pursuant to Section 29(1), delaying the submission of a VAT Return attracts an administrative fine of Rs. 1,000 per tax period or a percentage penalty calculated at 0.05% of the tax due per day, whichever amount is higher. Additionally, under Section 26, any delayed tax remittance or unpaid output tax balance incurs a mandatory interest charge of 15% per annum, compounded daily from the initial due date. Operating outside these frameworks prompts the IRD to suspend your digital billing system, freeze your corporate import-export permits, and block the issuance of your physical Tax Clearance Certificate (कर चुक्ता).